SVB, Bailouts, and How to Regulate Capitalism

The SVB bailout has made me very mad. Not because it is a particularly egregious bailout. Compared to the 2008 crisis, only depositors above the FDIC limit are getting bailed out. There is a lot of substantive debate about whether that is ok or not and what the consequences will be for how financial systems work. Bond and equity holders will probably eat it.

I am a bit more concerned about two other things. First is the possibility that the new Fed facility might offer soft duration insurance to banks, thereby letting them partially absorb the pain of rate hikes. That puts things into relief: the mechanism through which rate hikes lower inflation is by lowering the labor share. The second thing that makes me angry is that this was not necessary in the first place. We had a regulatory regime under Dodd-Frank that would have prevented this. However, in 2018, a bipartisan group of senators weakened Dodd-Frank to exclude regional banks from some of its liquidity requirements. SVB was one of the leading organizations lobbying for this change.

What angers me is that many intelligent people, including my dear friend and colleague Saule Omarova, warned that this would happen. As thanks, she got red-baited in front of the Senate. The real story was not that she had especially controversial ideas about the future of banking but that regional banks were very nervous about having a strict and responsible regulator at the OCC. Their association and, in particular, several democratic senators who pushed for deregulation were the ones that allowed the GOP floor show to go ahead and distract from the real issue at hand – whether regional banks like SVB would be strictly monitored and regulated.

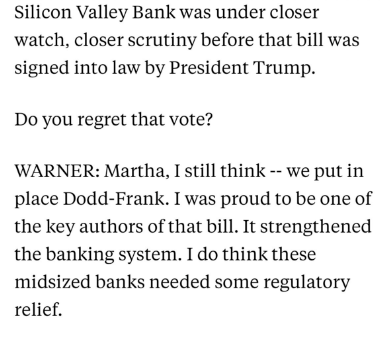

However, I do not write this blog to vent. Instead, I want to make some substantive points about why this keeps happening. The market economy, as we have structured it, requires banks to make credit available, and sometimes, that clashes with the need to protect depositors. A statement by one of those Democratic Senators responding to questions about his role in deregulating regional banks like SVB illustrates these tensions. In an interview with ABC, Mark Warner (D-VA) said this:

Regulator relief is a fun turn of phrase. It implies that if regulated similarly, mid-sized banks couldn't compete with larger ones. The problem here is that it is probably true that Dodd-Frank made mid-sized banks less competitive compared to GSIBs.

The relative contraction of regional banking under heavier regulation has material consequences for particular constituencies. Mid-sized banks are indeed very important to regional lending. Certainly, they might know a region better and serve their business customers well. We have a lot of evidence for this in how the Paycheck Protection Program (PPA) played out during the pandemic. The PPA program gave businesses loans to stay open, and if they kept their workforce on payroll, these loans would convert to grants. The program was administered through the Small Business Administration, which relied on private commercial banks to originate the loans. Studies have consistently found that small businesses which banked with smaller regional banks were able to have easier access to PPA loans. So when we look through the list of Democratic senators who voted for loosening Dodd-Frank, we don't just find your usual, bank-friendly customers like Warner but usually great Senators like Montana's John Tester, whose state is agricultural and does depend on regional, specialized lenders.

How are we to square this whole thing? The answer unsurprisingly lies with Hyman Minsky and Michal Kalecki. Minksy and Kalecki (the former of whom was a reader of the latter) show that in a capitalist system, growth is driven by investment, and private entrepreneurs primarily make investment decisions. To enable investment, we create a private banking system that issues credit. Credit allows us to take cash flows from the future and transport them into the present to fund the creation of capital assets which will create profits later. Banks will make that up by charging interest – a quasi-rent – from these future investments. However, you are in trouble if the future doesn't turn out as you thought. And so are the banks because they need those quasi-rents to pay out depositors. Thus, the Minksyian instability hypothesis and the "Minksy moment" when an investment cycle ends in a bank run.

However, in one of the best essays on Minksy, Mike Beggs points out that the Minksy moment is not the bank run but the bailout. Given its ability to issue money – the final means of settlement – the state makes someone whole and prevents the run. That allows us to stabilize investment and eventually write off the non-performing loans/depreciate the assets that they back. In the case of SVB, the whole thing is peculiar because it was not the loan book that was underperforming but rather that SVB would force their borrowers to be their depositors AND give them warrants on their company's equity to boot. This unpleasant business practice led many firms to pile up huge, FDIC uninsured deposits in SVB that go against normal cash management practices. So by making those deposits whole, the FDIC and the FED are doing something like a bailout of borrowers, not just depositors. They will likely wipe out the bank's equity and debt, which is good.

As you can tell, it's a mess. But Begg's larger point stands. The bailout is how modern capitalism deals with investment cycles through the state's intervention. And in doing so, the state assigns losses to someone. That's where the politics lie! This dynamic is especially vicious in the United States. As I like to tell my European counterparts, "America does social policy through investment and industrial policy." This means that the US has a very weak welfare state but is not a small state. The American government is very good at stimulating investment and cleaning up the consequences of bubbles. At its best, this makes the American economy extremely innovative and productive and creates many highly paid jobs and employer-provided benefits. However, at its worst, it leads to lost decades and massive inequality.

The Biden Administration's IRA is this American tradition at its best. It treats climate change as a problem of investment in the face of mild technological uncertainty. As such, it is trying to blow up a lot of what Bill Janeway has called "productive bubbles" to see what works. Along the way, IRA will create many well-paid jobs and employer benefits packages. This strategy is being played out in implementing the CHIPS Act, where funding recipients have certain standards for employee benefits like childcare. This is how America solves the issue of welfare state policy without a welfare state – through an industrial policy-driven bubble.

But as with any bubble, it will deflate. Again, the American state is very good at dealing with this damage. As we've shown repeatedly, we know how to backstop a financial system. That's the magic of America. However, the tools we developed to do so were constructed in ad-hoc ways in response to lots of crises and learning by doing. Thus, what we don't know how to do as well is to apply these mechanisms in a way that is pre-planned and explicit in how it distributes the downside.

This is where my friend Saule Omarova steps in! In her work with Robert Hockett and others, she has noted that the state is vital to the smooth functioning of the private banking system and its support for investment. So, she asks, why not make it official? Instead of an ad hoc bailout of real assets through a private financial system, which tends to be very indirect in its effect, why not have some public entities which can do the work directly? This is most explicit in work Saule, and I did together on a "bailout manager" whose job is to buy out the tangible assets of critical sectors facing bubble dynamics. However, this theme of recognizing the state's enablement of private investment and, thus, the need to have an explicit policy for managing the bailout and fallout of financial capitalism runs through all her work. And this recognition of capitalism's natural and normal functioning and how to make it more efficient apparently makes someone some raging Marxist...

The cherry on this cake is that the VCs who created hysteria about a relatively minor banking issue might have finally stepped in it. Senator Warner's statement on the whole mess blames a "reckless run" on SVB by depositors. I am sympathetic to his anger. Legal systems can only work if reckless actors are punished and over the past few years social media-savvy investors have floated all kinds of laws with little consequence. However, let's not kid ourselves. You risk this when you deregulate a piece of the banking sector. So while I think many of the Twitter-active VCs acted irresponsibly and perhaps committed some actual crimes, when made examples of by the Senate Banking Committee and the SEC, they will be covering up for the more significant mistakes that got us here.